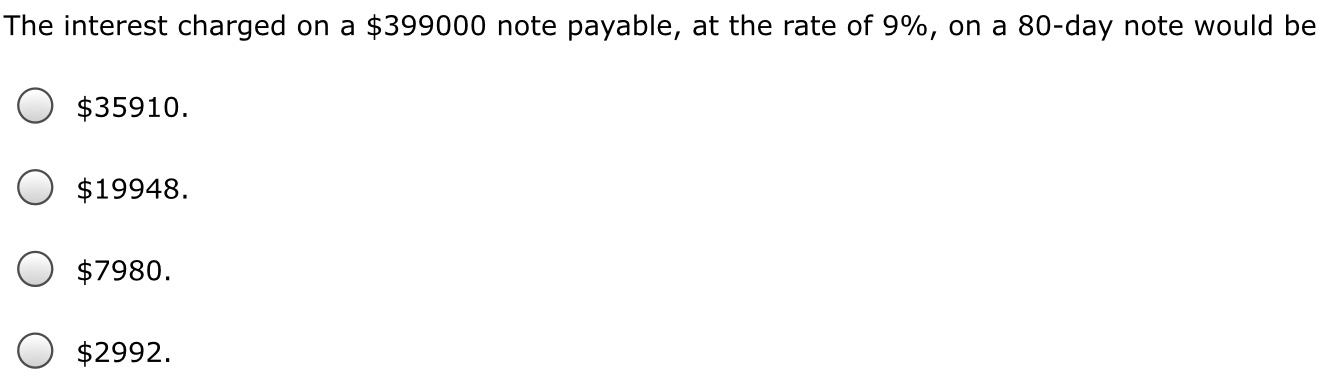

Online Order

Online OrderToday, mortgage brokers is actually perhaps among quickest and you will safest ways to buy a property. Everything you need to perform is to fill in needed data so you’re able to your chosen financial or loan company and fulfill the eligibility criteria. Bringing a mortgage is as simple as you to definitely however, using it back which have appeal for a period of 20-30 years ‘s the real thing, and also to succeed shorter difficult, many fiscal experts now suggest homebuyers to go for brand new pre-percentage of financial alternative.

- Start out with Quick Prepayments

- Choose for increased EMI>

- Higher Down-payment

- Help the EMI amount

- EMI fee

- Having fun with MFI/Bonds/RD/FD

Financial pre-fee mode settling the loan matter in a choice of area otherwise complete up until the structured period. This is how submit, whenever you are obtaining off loan personal debt. Doing so will help you slow down the financing name and/or EMI. On the other hand, this will help it can save you cash on the interest.

Suppose you’re taking a house out of ?fifty lakh to have a period of twenty five years, within an interest rate regarding 8%. In cases like this, your own month-to-month EMI would be to ?38,591. At the conclusion of the latest twenty five years, the quantity that you will have reduced as well as focus perform be available ?step 1.fifteen crore. Therefore, you are paying ?65.8 lakh just as notice!

Into the initially repayment decades, very individuals discover that the main amount gets paid off reduced. The first few age come down to simply paying rates of interest.

Using exact same analogy forward, in the 1st five-season period, you will simply pay eight.7% of the overall amount borrowed. Throughout the next four-12 months several months, up to 19.2% of one’s financing could well be reduced. After that, by the end of third five-year several months, doing thirty-six.4% mortgage might possibly be reduced and also by stop of your next five-12 months several months, it payment do boost to 61.9% of one’s overall number. Eventually, at the end of the fifth four-seasons months, the entire dominant number might be lso are-reduced. That is why you should invariably pre-romantic financial to get recovery towards the notice through to the main amount.

Suggestions for Foreclosures off Financial

The best way to foreclose financing is to try to create restrict repayments right away and you can completely personal they within a few decades. not, few finance companies and you may credit organizations can get levy specific fees to own very early foreclosures. Yet not, it is still great to blow the brand new punishment commission than just using the eye due to the fact at the very least, you’re obligations-100 % free and can purchase your bank account on almost every other essential things. Therefore, regardless if you are choosing full or area prepayment out-of an effective home loan, talking about some of the information that can come in handy:

- Start off with brief prepayments

- Opt for a top EMI

step 1. Focus on Quick Prepayments

One of the ways of pre-payment is to begin by lower amounts to start with, following aggressively boost they season-on-seasons in the a steady rate. This you certainly can do of the setting aside a certain amount through the the season, just for it objective.

dos. Decide for Highest EMI

Another a good option choice is to blow more compared to the EMI number, per month. This would demonstrably ount area by region and you can wade an extended method in lowering your debt.

step 3. Fixed Prepayment

For every year, you could potentially decide to pay a particular lump sum number. This needs to be significantly more than your EMI installment payments. This is why you could potentially pre-afford the dominating amount quickly.

4. Large Down payment

Financial experts strongly recommend the better advance payment system is certainly one of the best ways of home loan pre-payment. It’s got are done at the beginning, if you find yourself paying quite a bit of the borrowed funds. That it cuts a massive chunk on the prominent definition your loan label are now able to be less so that the rate of interest.

5. Increase the EMI matter

A great salaried body is more likely to score an annual boost on a yearly basis. It indicates extra income along the earlier in the day 12 months. Today, which extra earnings can be used to boost the EMI matter from the a small percentage. This may be a small step but can in the course of time aid in reducing the interest in the long run.

six. EMI commission

Along with annual raises, salaried people are also planning score specific bonuses out-of big date-to-date just like the a reward for their really works. Which extra number are often used to spend the money for most EMI one to pay the borrowed funds shorter and you can second to store with the the attention amount.

7. Using MFI/Bonds/RD/FD

Another way is to accrue a substantial amount to pre-shell out home financing through investing in mutual fund, securities otherwise by simply making recurring otherwise fixed deposit funds that have a keen try to make use of this readiness currency to have foreclosures of the property loan. Investing this type of profiles will not only save however, buy you notice with it that one may divert to help you repay the borrowed funds.

As to the reasons go for Mortgage Prepayment?

The best answer is saving towards desire however, here is much more so you can it. Prepaying home loans is most beneficial as after that you’re free of any financial baggage after in life. Imagine if there is a major health issue having any kind of your family representative? This becomes a crisis, and no-one would like to provide top priority towards financial EMIs. Advanced schooling of pupils is also a new grounds, where zero father or mother want to sacrifice because of monetary constraints. Later years is yet another aspect that cannot feel ignored, and you will anybody would wish to alive a financial obligation-free existence shortly after 60 as there could be zero circulate from income monthly.

For this reason, most people today are choosing the new foreclosure alternative remaining its coming obligations and you will will cost you in your mind. Yet not, you need to remember that in order to pay-off the borrowed funds amount you need not mortgage your valuable property at any offered area of energy. Pre-percentage off home is the most suitable choice having borrowers, but it should be done in a strategic and you will quick style.